This may be a dumb question, but any idea why the market is often surging in one direction or the other primarily starting at 3:30? It’s been more common than not lately, and is strong late market action in-and-of-itself an indicator of some sort?

August 2007

Monthly Archive

Mon 6 Aug 2007

Sun 5 Aug 2007

When is it time to take advantage of the downturn?

Posted by John under Discussion , Tactics[2] Comments

The equity markets right now are extremely volatile. The VIX has more than doubled just in the past few months, and this presents some opportunity if you’re willing to buy during the dips. Before I go further, let me be clear that I’m only considering buying broad market indexes when buying dips – not individual stocks or niche ETFs or mutual funds. I feel buying into dips is only advisable when considering a broad basket of equities. So, to simplify the discussion below, assume that we’re talking about the S&P500 only (although this should apply to any index funds, ETFs and mutual funds that focus on a large basket of equities) and that we’re discussing using market dips to augment long-term holdings only.

The 3-part question I’ve been grappling with is: (1) what constitutes an actionable dip, (2) when to exploit this dip, and (3) how much to invest in the dip. Volatility helps create really nice dip opportunities, but it requires some speed, available funds, and some previously determined strategy to effectively capitalize on volatility. (more…)

Sun 5 Aug 2007

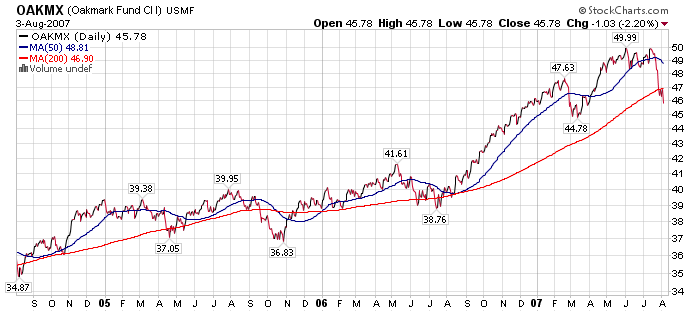

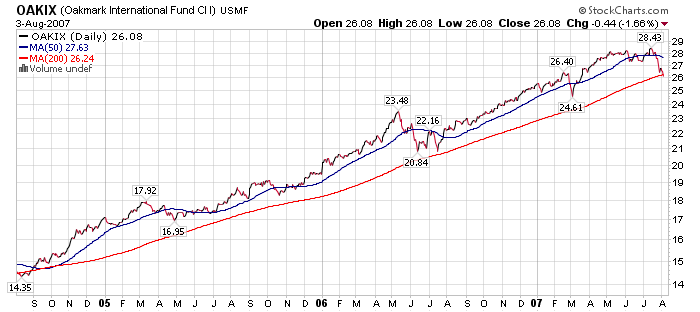

Quite a while ago, we discussed drawdown analysis for mutual funds, and how understanding drawdowns can help in setting properly positioned stop losses… With two of my mutual funds dropping down against their stop loss levels, it’s time to revisit the analysis.

We’re looking at OAKMX and OAKIX, both long term value oriented mutual funds run by Oakmark Funds. OAKMX focuses on large cap value; OAKIX focuses on large cap international value. Here are the 3 year performance charts of the two mutual funds:

Wow, good runs on both funds. (more…)

Sat 4 Aug 2007

If I Hear The Carry Is Dead One More Time…

Posted by Quicksilver under Commentary , Uberman's PortfolioNo Comments

You can’t click on a link on the net today, it seems, without coming across someone talking about the unraveling of the carry trade. Will the Japanese raise rates and end the party? Everyone knows that the ZIRP (zero-interest rate policy) of Japan is a major spark for carry trades since to have a carry you need one higher interest rate and one lower one to make it work. And zero is pretty low.

Everytime I hear?about it, I want to throw something. First of all, it’s a matter of principle. (more…)

Thu 2 Aug 2007

Here’s an interesting trick, in a roundabout explanation thanks to the latest GMO Quarterly Letter – investing without margin calls.

Imagine this, you’re a wealthy investor and have confidence in the long term growth of the economy and the markets. You want to get leveraged long as much as possible to benefit from this long term growth, but know that the inevitable dips and swoons are a threat to using too much margin.

Enter the concept of investing without margin calls. Think it’s not possible? Think again — it’s been happening at a record pace in the last year in the form of Leveraged Buy Outs (LBOs). The long-term investors who buy these companies are sometimes able to lever up as much as 10 to 1, so they might put up $100 million to buy a $1 billion company. They sell bonds (backed by the company’s assets and earning power) to cover the rest of the $900 million difference, and are able to get much more leverage than if they were simply getting 50% margin (2 to 1 leverage) from their stock broker.

But there are plenty of risks, such as the cost of? servicing all that debt, getting the company to grow as much as it would have under public ownership, etc.

It’s an interesting trick if you have enough money to pull it off.? It’s effectively a risk-reversal where the risk of a margin call is shifted from the equity owner to the debt buyer.

Wed 1 Aug 2007

Jim Cramer is nothing, if not attention getting. Here are two different videos from Jim on the subprime situation that are quite interesting… I have presented them in chronological order for effect. (more…)