Thu 12 Oct 2006

When working on my data for analyzing liquidity, I calculated the yield spread as TNX – IRX (10 year minus 3 month), where StockCharts provides an easy way to see TNX / IRX (10 year divided by 3 month)… and this got me thinking about my post a while ago on inflation expectations… it seems as though I may have made a minor mistake in my analysis… which leads to a major mistake in my conclusion. Mea culpa.

Instead of looking at the relative rates (division) of TLT and TIP as I did, I should have been looking at the difference in rates. And to make everything else more fun, it shows a contradictory path for inflation expectations than what I originally surmised…

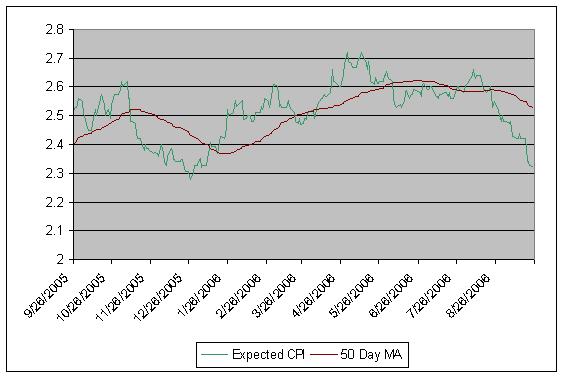

I pulled down the data for the real treasury rates (as opposed to TLT which is a proxy for the treasuries) and drew up the following chart as the difference between the traditional and inflation adjusted 10 year treasury rates. Since the traditional bonds shoudl include a premium for inflation expectations, taking the difference of the two implies what the expectation is for long term inflation. Remember, these are the 10 year rates, so the market would look past the problems or inflationary forces present in a shorter time frame.

So, in contrast to the TLT:TIP chart I talked about, inflation expectations have actually been falling since April, most likely in anticipation of a recession and/or the general faith in the Fed to keep inflation under control.

The chart of TIP:TLT (inverted from my original post) on StockCharts is a little closer to the above chart, though it is not perfect.

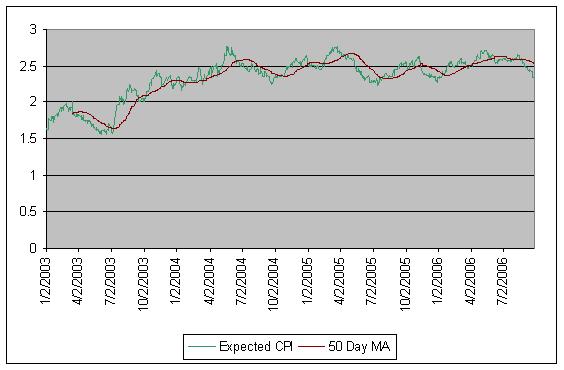

Inflation Adjusted Treasuries have had a short life so far, so it’s not too hard to see the entire history of this measure of expected inflation. Here is the chart since TIP data has been available in 2003:

I labelled the charts “Expected CPI” for a reason… the premium paid on the inflation adjusted treasuries is based on the CPI, not the actual rate of inflation. This is important as the CPI can be slightly divorced from reality.

You can also read a research paper from the Fed where they looked at the same data to measure Inflation Expectations.