David Einhorn has an interesting perspective on the current state of the world as he recently penned in a NY Times op-ed piece…

Are you worried that we are passing our debt on to future generations? Well, you need not worry.

We’ve made the problem so bad that our generation — not our grandchildren’s — will have to deal with the consequences.

The whole article is worth a read.

An amusing joke:

A Lehman Brothers’ lawyer takes a cab to the bankruptcy court. The cabbie says the fare is $27. The lawyer says, “Come inside and join the unsecured creditors.”

Here’s some more insightful analysis from “a young analyst” via Ritholtz:

It boils down to this: this episode exposed structural flaws in how a trade is implemented (think orphaned algo orders) and it exposed the danger of leaving market making up to a network of entities with no mandate to ensure the smooth and orderly functioning of the market (think of the electronic market makers and high freqs who can pull bids instantaneously as opposed to a specialist on the floor who has a clearly defined mandate to provide liquidity).

This is not the market of olde times… with effectively no market makers, an assumptions about liquidity and always having a bid to hit is now a dangerous assumption.

With this in mind, what are your options in the event of another no-bid situation?

- Buy and Hope (a.k.a. Buy and Hold) — don’t worry about needing to sell, believe in the underlying value of what you own or how the market is currently pricing that value.

- Stand aside whenever the volatility cranks up.

- Panic early and sell before everyone else sells, thus selling before the bids disappear. Note that this will create churn if you want to plunge back in quickly…

- Hedge your positions.

- Enter into married puts to protect your downside. This can be more effective than a stop order in an illiquid market, but carries its own associated costs.

- Put on some short positions to balance your long positions.

- Be prepared with a list of alternative ways to balance your long exposure. If INTC goes no-bid, can you short QQQQ instead? If you’re long PG, can you do a bullish option spread instead? Can you hedge an equity position with a forex trade?

- Are you prepared to buy when no one else does? Some low-ball bids for PG and similar stocks got filled, and the trades didn’t get busted… do you have the guts to buy during panic?

All this advice will work for those of us at the retail level… but there are serious issues for managers of mutual funds. In a market that is stacked against the smaller trader, this ability to be nimble is one of the few advantages to be had.

John Hussman starts his weekly commentary this week with two very timely quotes.

“Of all the mysteries of the stock exchange there is none so impenetrable as why there should be a buyer for everyone who seeks to sell. October 24, 1929 showed that what is mysterious is not inevitable. Often there were no buyers, and only after wide vertical declines could anyone be induced to bid … Repeatedly and in many issues there was a plethora of selling orders and no buyers at all. The stock of White Sewing Machine Company, which had reached a high of 48 in the months preceding, had closed at 11 on the night before. During the day someone had the happy idea of entering a bid for a block of stock at a dollar a share. In the absence of any other bid he got it.”

John Kenneth Galbraith, 1955, The Great Crash

“I started accumulating stocks in December of ’74 and January of ’75. One stock that I wanted to buy was General Cinema, which was selling at a low of 10. On a whim I told my broker to put in an order for 500 GCN at 5. My broker said, ‘Look, Dick, the price is 10, you’re putting in a crazy bid.’ I said ‘Try it.’ Evidently, some frightened investor put in an order to ‘sell GCN at the market’ and my bid was the only bid. I got the stock at 5.”

Richard Russell, 1999, Dow Theory Letters

May 6th’s flash crash was just this situation. Bids disappeared. When you have people, programs, or margin clerks conditioned to expect a liquid market, they might put in market orders when no bid exists…

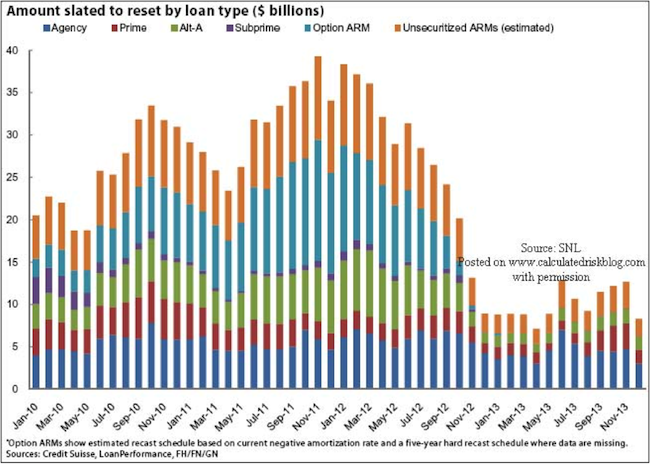

Here is the reset chart for mortgages again (click to zoom)… You might notice there is an increase looming over the next 6 months or so…

The timing of problems may be variable though as banks don’t seem to be eager to foreclose any more, and we have tons of policy makers trying to kick the can down the road a bit further (especially if they can postpone issues till after the election in November).

So, it started out as a bit of a down day, nothing crazy. And then around 2:40pm the bottom apparently fell out of the market. Dow down 998 points (give or take) before a V-shaped bounce back out of the crash to close down 348 points.

Apparently, the rumor at the time was that a trader at Citi fat-fingered a trade, putting a B in his sell order instead of an M, turning a million dollar trade into a billion dollar one. The interesting thing about that? Citi denies that anything like that happened. Third parties looked at the amount of volume Citi’s trading desk did, and said there was nothing unusual that could cause this kind of move.

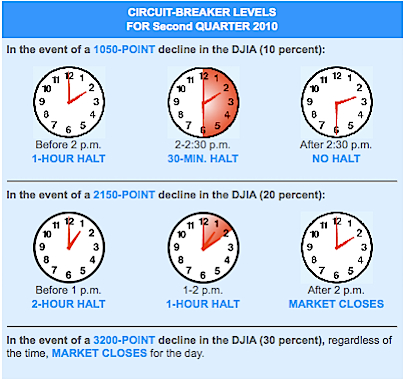

Regardless of cause, aren’t there some sort of circuit breakers for when the market drops too quickly? Well, the curbs start at 10%, and the 10% curb is not in effect after 2:30pm. Very interesting that the whole thing went down at 2:40pm.

(From NYSE).

Had the market free-falled to be down 20%, the NYSE would have closed trading, ideally so everyone can catch their breath and cooler heads prevail.

Zero Hedge intelligently thinks it was caused by High Frequency Traders (HFT) all acting in a negative feedback system:

…absent the last minute intervention of still unknown powers, the market, for all intents and purposes, broke. Liquidity disappeared. What happened today was no fat finger, it was no panic selling by one major account: it was simply the impact of everyone in the HFT community going from port to starboard on the boat, at precisely the same time. And in doing so, these very actors, who in over a year have been complaining they are unfairly targeted because all they do is “provide liquidity”, did anything but what they claim is their sworn duty.

In 20 minutes the market showed that it is as broken as it was at the nadir of the market crash. Through its inactivity to investigate the market structure, the SEC has made things a million times worse…

After today investors will have little if any faith left in the US capital markets, assuming they had any to begin with.

That last point is an important one. How many people will see today’s market behavior and decide to sell in their 401k? If we go down big into the weekend, are we setting ourselves up for another 1987 Black Monday Crash type event? (In case you didn’t know, the Thursday and Friday leading into the weekend were big down days, -2.4% and -4.6% respectively.)

On the flip side, those folks over at StockTwits have created a t-shirt to commemorate the brief crash…

My opinion? This market is basically fake… the melt-up that has been happening is a by-product of zero rates at the Fed and HFT trading… once some actual turmoil hits, all the bids disappear. There probably is no single cause for today’s plunge, other than down was the path of least resistance for the markets. HFT probably contributed to the plunge, and may have contributed to the recovery too.

Regardless of my opinions, today’s move is going to continue to chip away at the idea that the markets are fair, efficient, or even consistent.